What to Do If You Owe Taxes This Year

(And Can’t Pay in Full)

If you just finished your tax return and saw a balance due you can’t pay, take a breath.

You are not alone. Owing taxes is common. Not being able to pay the full amount immediately is even more common.

What matters now is what you do next.

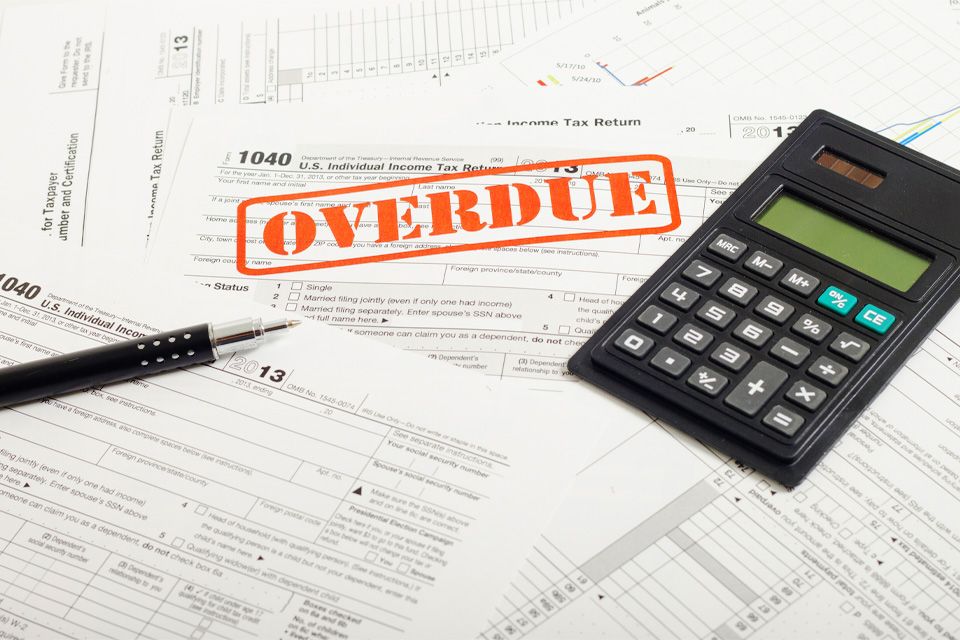

The worst move is not owing.

The worst move is ignoring it.

Here’s how to handle it the right way.

1. File Your Return — Even If You Can’t Pay

This is the most important step.

If you owe and don’t file, the IRS charges a failure-to-file penalty, which is significantly higher than the failure-to-pay penalty.

- Failure to file: up to 5% per month.

- Failure to pay: generally 0.5% per month.

Filing protects you. Avoiding makes it worse.

Even if you can only pay a small portion right now, submit the return. It stops the largest penalties from piling up.

Extensions do not extend payment deadlines. If you owe, the balance starts accruing interest after the due date whether you file or not.